Inheritance Tax – Taper Relief & Gifting allowance:

Inheritance and the associated tax implications may not be something that you are familiar with or concerned with yet, however with careful planning there are ways of ensuring that the tax payable on possessions passed on to your beneficiaries are minimised.

Under current legislation, Inheritance Tax (IHT) is payable on the total value of your estate that exceeds the current £325,000 Nil Rate Band (NRB) at a rate of 40%.

Taper Relief

There are ways however to reduce the rate of IHT charged on gifts before you die depending on when the gift was made. This is known as Taper Relief.

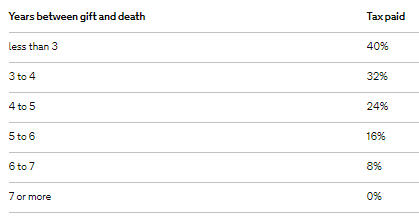

The amount of tax payable on gifts is restricted based on the total time that has passed between the date the gift was made and date the person died.

If the donor dies between three and seven years after making a gift and the total value of gifts made is over the NRB, the amount of IHT is reduced on a sliding scale as seen below:

If seven years pass since the donor makes the gift and they have not yet died, then the gift falls outside of their estate and no IHT falls due.

It is important to note that Taper relief is only applicable to gifts and only comes into play when the total cumulative value of gifts made prior to the death of the donor exceeds the current NRB.

Taper relief can prove to be very useful if you intend to make large gifts and wish for the IHT tax burden falling on your beneficiary to be reduced.

Annual exemption:

Whilst you are alive, you are also able to gift up to £3,000 worth of cash or certain assets each tax year, without it being added to the value of your estate for IHT purposes. This is known as your annual exemption or gift allowance.

Any unused portion of this allowance can also be carried forward to the following year but only for a single year.

For more information about what qualifies as a gift, what gifts are permissible under the gifting allowance, other types of exempt gifts or for any general enquiries about Inheritance Tax please do get in touch or follow the link below:

You may also like…

Inheritance tax planning

Gift aid donations

60% pension relief

What are self-assessment tax returns?

CGT update

Student loans

I have no use for bodyguards, but I have very specific use for two highly trained certified public accountants.

Elvis Presley