How to write off Bad Debts within QuickBooks Online (QBO)

Bad debt(s) will mean that a customer owes you money, however for some reason you are unable to collect it. Within QBO, this will result in you having a debt owed to you which you know you aren’t going to get paid for. To write this balance, or ‘bad debt’ off, the remaining balance will need to be cleared by creating a credit note. This will enable you to clear the ‘bad debt’ off which will most likely still be shown outstanding on an invoice (which QBO believes the customer still owes). By doing so, this process will ensure that your accounts receivable and net income stay up to date. The process to write off ‘bad debts’ is shown below through four easy steps:

- Firstly, you will need to have a bad debt expense account set up within your QBO. If you haven’t already, the process to do so is to locate the Accounting tab on the left hand menu and then select Chart of Accounts. You will need to select the account type to ‘Expense’ and the detail type to ‘Bad Debts’. After this, you can proceed to save and close which will set up the account ready for use.

- The next stage will be to create a ‘Bad Debt’ item within QBO if you have not done so already. This can be attained by heading towards ‘Settings’ in the top right-hand side and then selecting ‘Product and Services’. From here, you will need to select ‘New’ on the right-hand side and then ‘Non-Stock’. In the ‘Name’ field, enter ‘Bad Debts’ and from the Income Account, select ‘Bad Debts’ as seen below.

You can then hit ‘Save and Close’.

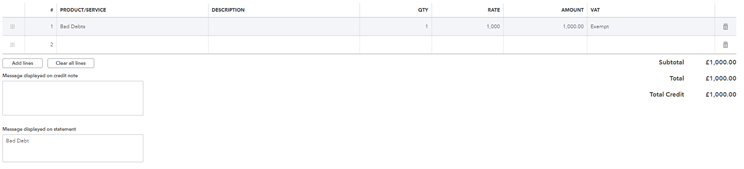

3. The next stage will be to create a credit note for the bad debt. This can be carried out by selecting ‘New’ within the top left of QBO, and then selecting ‘Credit Note’ which is located under the customer dropdown. From here, you will be able to select the customer for who the bad debt will need to be applied to from the ‘Customer dropdown’, and within the ‘Product/Service’ section select ‘Bad Debt’. From here, you can proceed to enter the amount you would like to write off as seen below for an amount of £1000. For good practice, you can always enter a display message ‘Bad Debt’, so you are aware what the credit note relates to for future reference.

After selecting the attributed VAT rate, you can select ‘Save and Close’.

4. The fourth and final step will be to apply the newly created credit note to the invoice in order to write it off. This is achieved by finding the invoice and then clicking on ‘Receive Payment’. In the receive payment screen, at the bottom you can tick the credit note created in step three and save the payment.

If you want to get the most out of your QuickBooks account, you can book a training session with a member of our Cloud Management Team.

Contact

You May Also Like…

Beware of little expenses; a small leak will sink a great ship.

Benjamin Franklin